Let’s learn how to invest $100,000 in U.S. real estate in 2026. Rental properties, REITs, crowdfunding, leverage strategies, and capital gains tax explained.

Let’s start with something most real estate articles won’t tell you upfront.

A hundred thousand dollars will not buy you a house in San Francisco, Austin, or Miami Beach in 2026. Not even close. But that same $100,000 can absolutely get you into the real estate market, sometimes into multiple properties. if you understand how the current market actually works and where the real opportunities are sitting right now.

This is not a “get rich quick in real estate” article. Those don’t work. What follows is a grounded, practical breakdown of exactly what $100,000 can do in U.S. real estate in 2026 . the strategies that make sense, the ones that carry risk, and why this particular moment might be better for new investors than the past three years combined.

What the 2026 U.S. Real Estate Market Actually Looks Like

Before putting a dollar into any property, you need to understand the landscape.

Mortgage rates are expected to hover around 6.3% for 2026 . slightly lower than the 6.6% average seen in 2025. While that’s still elevated by historical standards, the drop is meaningful because lower rates translate to larger buying power for investors. Fortune

Zillow projects home values will rise 1.3% nationally in 2026, with existing home sales climbing to approximately 4.267 million, a 4.4% increase over 2025 . as improving affordability pulls more buyers back into the market. State Street

J.P. Morgan’s global research team takes a more cautious view, forecasting U.S. house prices to stall near 0% growth in 2026, with a slight improvement in demand likely offsetting any increased supply. Swiss America

Here’s what that conflicting data actually means for a $100,000 investor: you’re not entering a boom market, and you’re not entering a collapsing one either. A housing market crash is not on the horizon .$36 trillion in homeowner equity and tight lending standards make a 2008-style collapse unlikely. This is a stabilizing market . which is actually one of the best environments for disciplined, long-term investors to enter without competing against the panic-buying frenzy of 2021 and 2022. Yahoo Finance

Emerging Midwest markets are showing particular strength in 2026. Columbus, Ohio, Indianapolis, and Kansas City are experiencing outsized growth driven by affordability, proximity to major universities, and steady population inflow. These are the kinds of markets where $100,000 goes furthest. NerdWallet

If you’re planning to invest $100,000 in real estate, 2026 offers…”

Strategy 1: Down Payment on a Single-Family Rental . the Foundational Move.

“Invest $100,000 in U.S. real estate.“

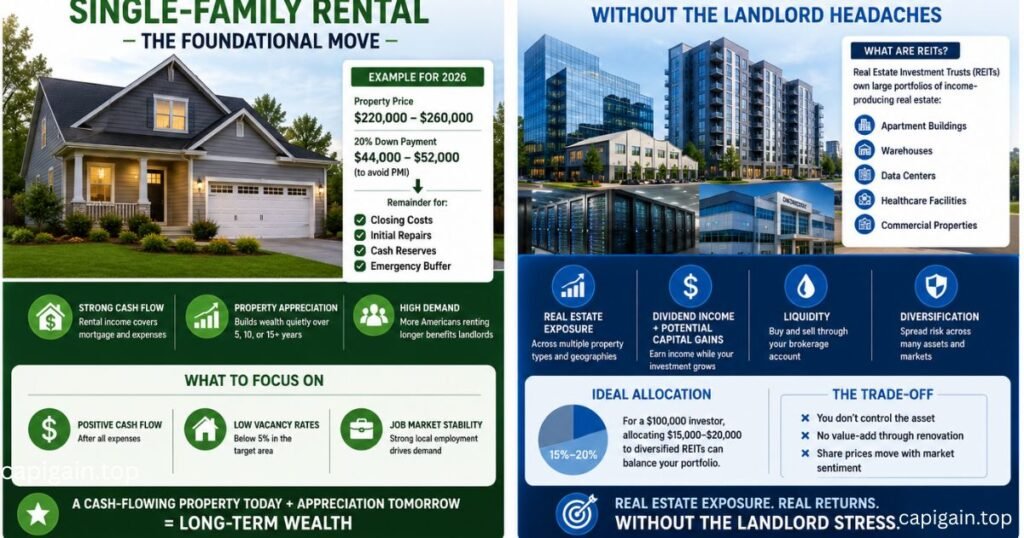

If you want real estate exposure with hands-on control, using $100,000 as a down payment on a single-family rental property in an affordable, growing market is still one of the most reliable capital gain strategies available to individual investors.

Here’s a realistic example for 2026. A property in Indianapolis or Columbus priced at $220,000–$260,000 requires a 20% down payment roughly $44,100–$52,100 to avoid private mortgage insurance. That leaves you with meaningful cash reserves for repairs, vacancies, and carrying costs. The remaining $100,000 can fund the down payment, closing costs, initial repairs, and a proper emergency buffer.

Single-family rentals are particularly well-positioned through at least 2027, while multifamily faces some oversupply pressure working through the system. High ownership costs and persistent mortgage rates are keeping more Americans renting longer . which directly benefits landlords. Yahoo Finance

The capital gain story with rental property is a two-part equation: monthly rental income that covers your mortgage and expenses, plus property appreciation building quietly in the background over five, ten, or fifteen years. Neither piece alone makes you wealthy. Both together, over time, absolutely can.

What to focus on when evaluating rental properties: positive monthly cash flow after all expenses, vacancy rates below 5.1% in the target area, and job market stability. A property that cash-flows even modestly in year one is almost always preferable to a speculative buy in a trendy market.

Strategy 2: REITs Real Capital Gains Without the Landlord Headaches

Not every investor wants to deal with tenants, maintenance calls, or property managers. If that sounds like you, Real Estate Investment Trusts REITs offer genuine real estate capital gain exposure through a standard brokerage account.

REITs own large portfolios of income-producing real estate: apartment buildings, warehouses, data centers, healthcare facilities, and commercial properties that most individual investors could never access directly. You buy shares the same way you’d buy stock in Apple or Amazon.

CBRE’s 2026 market outlook notes this is an opportune time to realize gains from existing real estate investments and redeploy capital; pricing currently offers legitimate opportunities that weren’t available during the overheated years of 2021 and 2022. U.S. Gold Bureau

For a $100,000 investor, allocating a portion, say $15,100–$20,100, to diversified REITs provides real estate exposure across multiple property types and geographies without concentration risk. You get dividend income, potential capital gains, and liquidity that physical property simply cannot match.

The trade-off,

You don’t control the asset, you can not add value through renovation, and share prices move with market sentiment in ways that don’t always reflect underlying property values.

3: Real Estate Crowdfunding. Access to Deals You Couldn’t Touch Alone

Over the past decade, real estate crowdfunding platforms have grown from a niche concept into a legitimate investment channel. Platforms like Fundrise, CrowdStreet, and RealtyMogul allow investors to pool capital and participate in commercial, residential, or mixed-use projects that would normally require institutional capital.

For a $100,000 budget, crowdfunding can provide something difficult to achieve any other way: diversification across multiple projects, markets, and property types simultaneously. Instead of concentrating everything in one rental property in one city, you might spread $30,100 across six different projects in different states.

The capital gains potential here comes from project-level appreciation and profit distributions when properties are sold. Hold periods typically run three to seven years. Liquidity is limited during that window, so this works best as a medium-term allocation within a broader investment strategy rather than your entire $100,000.

4: The Leverage Play: 2 Properties Instead of 1.

Experienced investors often look at a $100,000 budget differently than beginners do. Instead of one property purchased with minimal debt, they use leverage to control more assets.

Using $100,000 strategically across down payments on two properties. Each priced around $200,000–$230,000, it doubles your exposure to rental income and property appreciation simultaneously. Both properties are building equity, both are generating rental income, and both are compounding capital gains over time.

The math is compelling when markets perform well. The risk is equally real when they don’t. Leverage accelerates both gains and losses. 2 properties also mean two sets of maintenance costs, two tenant relationships, and 2 mortgage payments to cover during vacancies.

This strategy makes sense for investors who already understand property management .or who have a reliable property manager . and have enough financial stability to carry both properties through a difficult quarter without stress.

Understanding Capital Gains on Real Estate , What You Actually Keep

Generating a capital gain on real estate is one thing. Understanding what the IRS takes is another conversation entirely.

When you sell a U.S. investment property for more than you paid for it, that profit is a taxable capital gain. Properties held longer than one year are taxed at long-term capital gains rates of 0%, 15%, or 20% depending on your income bracket. Properties sold within a year are taxed as ordinary income, which can reach 37%.

Two powerful tools help investors legally reduce or defer capital gains tax. A 1031 exchange allows you to sell one investment property and roll the proceeds into another qualifying property without paying capital gains tax at the time of the sale .deferring that obligation potentially for decades. Depreciation deductions on rental properties also reduce your taxable income each year during ownership, meaningfully improving real after-tax returns.

These aren’t loopholes .They are established parts of the U.S. tax code designed specifically for real estate investors. Understanding them before you invest is the difference between a good return and a great one.

Where Smart Investors Are Looking in 2026

If location is the oldest rule in real estate, the 2026 version of that rule points toward affordability combined with economic momentum.

Inventory of homes on the market in April 2026 was 4.7% higher than a year earlier .still well below pre-2020 levels, but improving. That growing inventory is concentrated in markets where new construction has outpaced demand. parts of Texas and Florida in particular. Meanwhile, Midwest and Southeast markets with strong employment bases and relatively affordable price points continue to attract both residents and investors. Empower

The investor’s question isn’t “where is the most exciting market?” It’s “where does the math work?” Positive cash flow, manageable purchase prices, and populations that are growing not shrinking, are the three filters that matter most at any price point.

Final Thought: $100,000 Is a Foundation, Not a Finish Line

The investors who build serious wealth in real estate rarely do it with one transaction. They do it with a first transaction, then a second, then a third, each one funded partly by the equity and income generated by what came before.

Your $100,000 in 2026 is not your entire real estate career. It’s the beginning of a capital gain compounding process that, managed with patience and discipline, has the potential to look very different ten or fifteen years from now.

Research the markets. Understand your financing options. Know your tax obligations before you buy. And if you’re serious about building long-term wealth through property, treat every decision like the beginning of something larger. because it is.

For more capital gains guides on gold, crypto, and real estate investing, visit Capigain.top

Financial Disclaimer: This article is published by Capigain.top for informational purposes only and does not constitute financial, tax, or investment advice. Real estate markets vary significantly by location, and conditions change over time. Always consult a qualified financial advisor or tax professional before making investment decisions.

Thanks for visiting the campaign.top

Muhammad Qaisar is the founder and lead researcher at Capigain.top, a financial education platform dedicated to helping everyday people understand capital gains across cryptocurrency, real estate, gold, and agricultural investments. With a passion for making complex financial topics simple and accessible, Muhammad writes in-depth, research-backed guides that help readers make smarter investment decisions. He believes that financial knowledge should be available to everyone, not just experts.