Let me tell you about a guy named Marker. how to avoid capital gains tax on gold in the US

Marker is a 54-year-old school teacher from Ohio. A few years ago, he bought some gold coins not a massive investment, just a few hundred dollars here and there. He was not a professional investor. He was just trying to protect his savings from inflation the way his grandfather once told him to.

Fast forward to 2024. Gold prices had gone up. marker decided to sell. He made a decent profit around $4,100.

Then tax season arrived.

His accountant told him he owed 28% on that gain. Marker nearly choked on his coffee. He had no idea gold was taxed differently from regular stocks. He thought a profit was a profit , you pay your standard rate and move on.

He was wrong. And it cost him over a thousand dollars he wasn’t expecting to pay.

This article is for everyone who doesn’t want to be Marker.

First, Why Is Gold Taxed So Harshly?

Here is something most beginners do not know.

The IRS does not treat gold like a stock or a mutual fund. It treats gold like a collectible, in the same category as rare coins, antiques, and fine art.

And collectibles, under US tax law, are taxed at a maximum rate of 28% for long-term capital gains.

Compare that to regular long-term stock gains, which are taxed at 0%, 16%, or 21% depending on your income. Gold sits in a different, higher bracket.

So if you held your gold for more than a year and you’re in a higher income bracket, you could owe up to 28% on your profit. If you sold before a year was up, it goes into your ordinary income which could be even higher.

For someone in the Gulf or South Asia reading this: think of it like this. In many countries, if you sell property, you pay a “transfer tax” or “gain tax” to the government. The US does something similar with gold. The difference is that gold gets its own special, higher rate compared to other investments.

Now, the question is ,can you legally reduce or avoid that tax?

Yes. Here’s how.

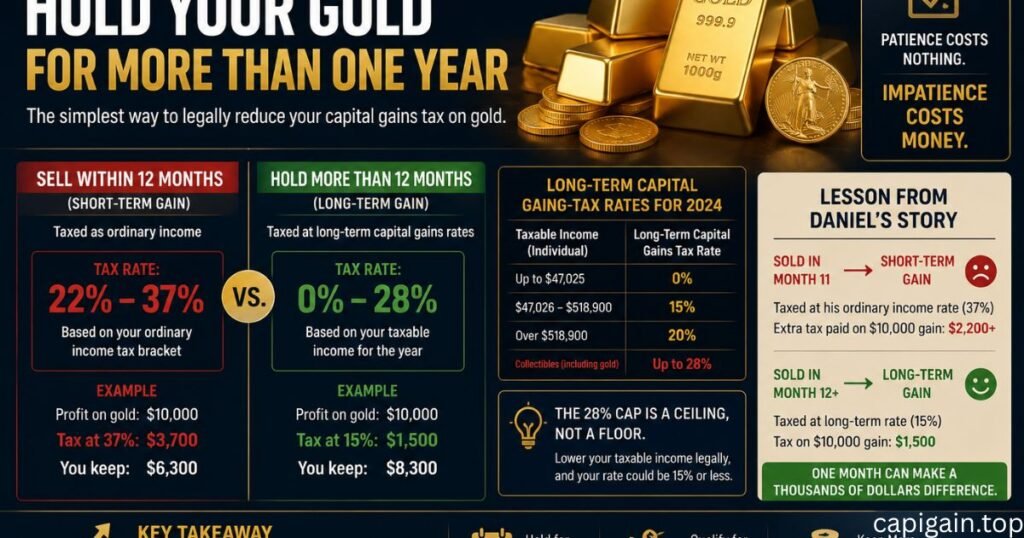

Strategy 1: Hold Your Gold for More Than One Year: How to avoid capital gains tax on gold in the US

This sounds almost too simple. But it works, and a surprising number of beginners miss it.

If you sell your gold within 12 months of buying it, the IRS taxes your gain as ordinary income. For most working Americans, that’s a 22% to 37% rate. That’s painful.

But if you wait more than 12 months, you qualify for long-term capital gains rates, which for gold max out at 28%.

Now, 28% isn’t great. But it’s better than 37%.

And here’s the real win. If your total taxable income for the year is low enough, your long-term gold gains might be taxed at 15% or even less. The 28% cap is a ceiling, not a floor.

So before you sell, ask yourself, how long have I held this? If you’re close to the 12-month mark, waiting a few more weeks could save you real money.

Lesson from Marker’s story: He sold in month 11. One month too early. He fell into the short-term bracket and paid his full ordinary income rate. Patience costs nothing. Impatience cost Marker extra.

Strategy 2: Sell in a Year When Your Income Is Lower

Timing matters more than most people realize.

If you know you’re going to have a low-income year ,maybe you’re between jobs, you took a sabbatical, you had large deductions, or you are retired with modest withdrawals , that’s actually a great year to sell your gold and lock in gains.

Here’s why. The IRS calculates your capital gains tax based on your total taxable income for that year. If your income is low enough, your long-term capital gains rate drops significantly.

Practically speaking, a single person in the US with a taxable income under about $47,000 in 2026 could pay 0% on long-term stock gains. Gold does not qualify for the 0% bracket the same way, but a lower income still pushes your gold gains into a lower effective tax zone.

For international readers, this is the equivalent of planning a property sale during a year you had fewer earnings ,intentionally choosing the timing of your transaction to minimize the tax bite.

It’s not cheating. It’s planning. The IRS expects you to do this. Every good accountant does it.

Strategy 3 , Use a Self-Directed IRA to Hold Gold

This one is a bit more advanced, but it’s legal and widely used.

A Self-Directed IRA is a type of retirement account in the US that allows you to hold physical gold and other alternative assets inside it. Regular IRAs only let you hold stocks and mutual funds. A Self-Directed IRA is different.

Here is the benefit. Inside a Traditional IRA, your gold grows tax-deferred. You don’t pay any capital gains tax when you sell the gold inside the account. You only pay income tax later when you withdraw the money in retirement and by then, your income is usually lower.

Inside a Roth IRA, it gets even better. Your gold grows completely tax-free. When you sell the gold inside a Roth IRA and eventually withdraw the profits in retirement, you pay zero tax. Nothing.

Think about that. You could watch gold double in value and owe the IRS absolutely nothing on that gain ,as long as it’s inside a Roth IRA and you follow the withdrawal rules. capigain.top will help you to follow the rule of law,

There are rules and limits to how much you can contribute each year, and you need to use an approved custodian to store the gold. But for long-term investors, this is one of the most powerful legal strategies available.

For Gulf and South Asian readers:

This is somewhat similar to a provident fund or pension scheme in your country ,money set aside in a special protected account that grows with tax advantages. The difference is you’re choosing to put gold inside it instead of just cash.

Strategy 4 , Offset Gold Gains with Capital Losses

This strategy is called tax-loss harvesting, and it’s one of the most common tools used by investors worldwide.

Here’s how it works. If you have other investments that have gone down in value, stocks, crypto, or other assets, you can sell those losing investments in the same tax year as your gold sale. The losses cancel out the gains.

Let’s say you made $3,000 profit selling gold. But you also have a crypto investment that’s down $2,000. If you sell that crypto and realize the $2,000 loss, your taxable gold gain drops to just $1,000.

You have cut your tax bill by two-thirds, legally.

The IRS allows you to use capital losses to offset capital gains dollar for dollar. And if your losses are larger than your gains, you can even carry them forward to future tax years.

One thing to watch: there is a “wash sale” rule for stocks, which says you can’t buy the same stock back within 30 days of selling it for a loss. However, as of current IRS rules, this wash sale restriction does not apply to gold or crypto, giving investors more flexibility.

This is practical for anyone, anywhere. If you hold a mix of assets, look at your whole portfolio before you sell gold. Selling a losing investment at the same time as your winning gold position is just smart math.

Strategy 5: Give Gold as a Gift: How to avoid capital gains tax on gold in the US

If you have gold and you want to pass it on to family without triggering a huge tax event, gifting is an option worth understanding.

In the US, you can give anyone up to $18,000 worth of gold per year (as of 2024 limits) without either of you owing gift tax. If you’re married, you and your spouse together can gift up to $36,000 per recipient per year.

Here’s the benefit. When you give gold as a gift, you’re not selling it. There’s no sale, so no capital gains tax is triggered for you at the time of the gift.

The person who receives the gift inherits your cost basis ,meaning if they later sell it, they’ll be taxed on the gain from your original purchase price. But if you’re giving it to someone with a lower income, their tax rate on that eventual sale might be much lower than yours.

And for gold passed down through inheritance (not a gift while you’re alive, but left in a will), the rules get even better. Inherited gold gets what’s called a “stepped-up basis,” meaning the recipient’s cost basis is reset to the market value at the time of your death. If they sell it shortly after inheriting it, they may owe little to nothing in capital gains tax.

Families who understand this rule save enormous amounts of tax across generations.

Strategy 6: Donate Gold to Charity

This one surprises people.

If you donate appreciated gold to a qualified charity, you avoid paying capital gains tax entirely on the appreciated value. And you may also get to deduct the full fair market value of the gold as a charitable contribution on your tax return.

It’s a double benefit. No capital gains tax owed. A deduction that reduces your other income.

This only works with IRS-qualified charities, and there are limits to how much you can deduct in a single year. But for people who plan to donate anyway, donating gold directly , instead of selling it and donating cash is almost always the smarter move.

What Does Not Work: Mistakes to Avoid

Let’s talk about what people try that gets them in trouble.

Some people think that if they convert gold to jewelry and sell the jewelry, they avoid the tax. They don’t. The IRS still considers it a sale of a collectible.

Some people think that trading one gold coin for another gold coin is not a taxable event. It is. Unlike real estate, which has a 1031 exchange rule allowing like-kind swaps without immediate tax, gold does not qualify for 1031 exchanges under current law.

Some people think that buying gold overseas and selling it there means the IRS won’t know. This is a dangerous assumption. If you’re a US citizen or green card holder, you owe US taxes on worldwide income, regardless of where the transaction happens.

And some people simply forget to report small gold sales, assuming the amounts are too small to matter. Every sale is reportable. The IRS cross-references dealer reports. It’s not worth the risk.

A Practical Checklist Before You Sell

Before you sell any gold, run through these questions quickly.

Have you held it for more than 12 months? If not, consider waiting.

Is this a high-income year for you? If yes, can you wait until next year when your income will be lower?

Do you have any capital losses in other investments you could realize at the same time?

Is the gold held inside an IRA or retirement account? If not, could it have been?

Are you planning to donate or gift some of this gold anyway?

If even one of these applies, you likely have a way to reduce what you owe.

Final Thought

Gold is one of the oldest forms of wealth in the world. People in the US, UK, Gulf countries, India, and Pakistan across cultures and generations ,have trusted gold to protect their savings.

But in the modern financial system, holding gold comes with rules. And the people who understand those rules keep more of their profits. The people who do not pay the Daniel tax.

None of these strategies require you to be rich or have a fancy accountant. They require you to plan ahead. Read the rules. Think before you sell.

Gold doesn’t expire. Your tax planning window does.

Disclaimer

This article is for educational purposes only and does not constitute tax advice. Please consult a licensed tax professional for your specific situation.

Thanks for visiting Capigain.top

Muhammad Qaisar is the founder and lead researcher at Capigain.top, a financial education platform dedicated to helping everyday people understand capital gains across cryptocurrency, real estate, gold, and agricultural investments. With a passion for making complex financial topics simple and accessible, Muhammad writes in-depth, research-backed guides that help readers make smarter investment decisions. He believes that financial knowledge should be available to everyone, not just experts.