Converting Bitcoin to Ethereum triggers a taxable capital gain in 2026 . even without touching US dollars. Learn exactly how the IRS calculates your income for capital gain, what records you need, and how to legally reduce your tax bill on crypto to crypto conversions.

I think that most people assume that converting Bitcoin to Ethereum is not a taxable event because they never actually received any US dollars in this way. That assumption costs thousands of investors real money every single year. The IRS does not care whether cash ever appeared in your bank account. The moment you disposed of Bitcoin regardless of what you received in return . a taxable event occurred. In 2026, with Form 1099-DA now reporting your transactions directly to the IRS, this is no longer a grey area that gets quietly overlooked.

This guide explains exactly what happens to your crypto capital gain when you convert Bitcoin to Ethereum, how to calculate what you earn. and three legal strategies that can significantly can reduce your tax bill.

What This Guide Covers in This Campaign. top research, “Crypto Capital Gain When You Convert Bitcoin to Ethereum”

- Does Converting Bitcoin to Ethereum Trigger a Tax?

- How the IRS Actually Sees a Crypto to Crypto Swap

- How to Calculate Your Capital Gain .Step by Step With Real Numbers

- Short-Term vs Long-Term: Why the Timing of Your Swap Matters

- What Records You Must Keep for Every Conversion

- Three Legal Ways to Reduce Your Tax on Crypto Conversions

- DeFi Swaps .Are They Different From Exchange Swaps?

- What Most People Get Wrong About This Rule

- Frequently Asked Questions

- Does Converting Bitcoin to Ethereum Trigger a Tax?

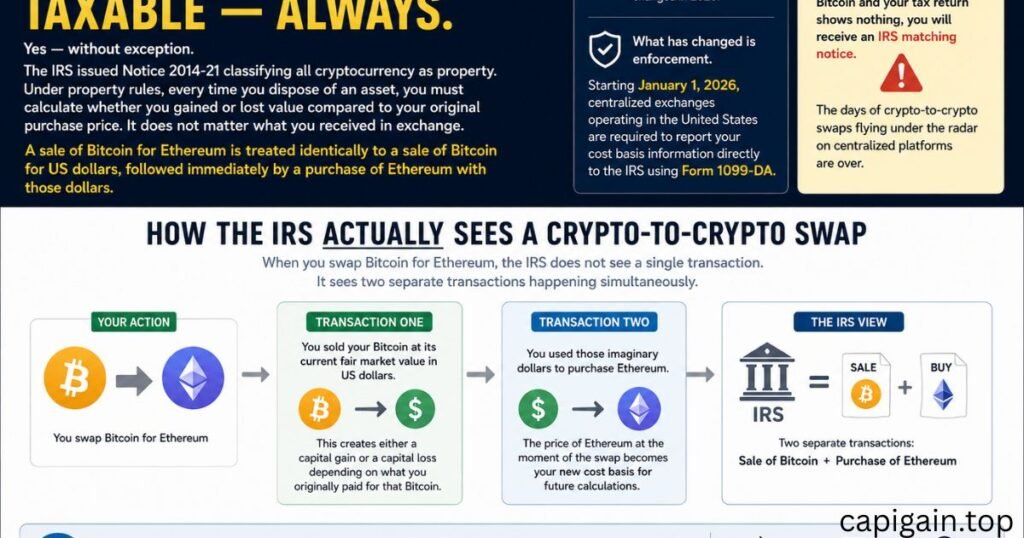

Yes without exception.

The IRS issued Notice 2014-21 classifying all cryptocurrency as property. Under property rules, every time you dispose of an asset, you must calculate whether you gained or lost value compared to your original purchase price. It does not matter what you received in exchange. A sale of Bitcoin for Ethereum is treated identically to a sale of Bitcoin for US dollars, followed immediately by a purchase of Ethereum with those dollars.

This rule has been in place since 2014 and has not changed in 2026. What has changed is enforcement. Starting January 1, 2026, centralized exchanges operating in the United States are required to report your cost basis information directly to the IRS using Form 1099-DA. If Coinbase reports that you swapped $45,000 worth of Bitcoin and your tax return shows nothing, you will receive an IRS matching notice. The days of crypto-to-crypto swaps flying under the radar on centralized platforms are over.

- How the IRS Actually Sees a Crypto to Crypto Swap

Understanding the IRS perspective here is what makes this rule click for most people.

When you swap Bitcoin for Ethereum, the IRS does not see a single transaction. It sees two separate transactions happening simultaneously.

Transaction One: You sold your Bitcoin at its current fair market value in US dollars. This creates either a capital gain or a capital loss depending on what you originally paid for that Bitcoin.

Transaction Two: You used those imaginary dollars to purchase Ethereum. The price of Ethereum at the moment of the swap becomes your new cost basis for future calculations.

This is not a technicality or a loophole. It is the fundamental structure of how property-based taxation works, and it applies to every crypto to crypto trade regardless of which coins are involved, which platform you use, or whether the swap took two seconds on a DEX or two minutes on a centralized exchange.

- How to Calculate Your Capital Gain , Step by Step With Real Numbers

The calculation follows the same formula used for any capital gain:

Capital Gain =

Fair Market Value at Swap . Original Cost Basis

Here is a realistic 2026 example that walks through the full calculation.

Situation:

You bought 1 Bitcoin in January 2024 for $45,000. You paid a $37 exchange fee when you bought it. Your cost basis = $45,035.

In April 2026, Bitcoin is trading at $89,000. You swap your 1 BTC for 29.5 ETH (because ETH is priced at approximately $3,088 each). You pay a $23 fee on the swap.

Your Capital Gain Calculation: Fair market value of Bitcoin at swap: $89,000 Minus your original cost basis: $45,035 Minus the swap fee: $23 Your capital gain = $48,943

This $48,943 is a taxable gain on your 2026 federal return , even though you never touched a single US dollar and you still hold cryptocurrency.

Your New Ethereum Cost Basis: The 29.5 ETH you received carries a cost basis of $89,000 , the fair market value of the Bitcoin you gave up. If Ethereum rises to $5,000 in the future and you sell, your gain on the Ethereum will be calculated from this $89.000 starting point, not from what ETH was worth on the day it was created.

- Short-Term vs Long-Term: Why the Timing of Your Swap Matter

The single most impactful variable in your crypto capital gain calculation is not the size of your gain .it is how long you held the Bitcoin before swapping it.

If you held Bitcoin for 12 months or less before the swap, your gain is classified as short-term. Short-term gains are taxed as ordinary income at rates up to 37 percent depending on your total annual income.

If you held Bitcoin for more than 12 months before the swap, your gain is classified as long-term. Long-term gains are taxed at 0, 15, or 20 percent depending on your income level.

Real Impact on the $46,943 Gain From the Example Above:

If held less than 12 months and income is $81,000: taxed at 22 percent . tax bill of approximately $10,107

If held more than 12 months and income is $81,000: taxed at 15 percent , tax bill of approximately $6,891

Difference from waiting past the 12-month mark: $3,316 saved on a single swap.

This is why the date you purchased your Bitcoin matters just as much as the date you convert it. One day past the 12-month mark transforms your entire gain from short-term treatment into long-term treatment. Many investors who swap at month 11 lose thousands of dollars they could have saved simply by waiting a few more weeks.

- What Records You Must Keep for Every Conversion

With Form 1099-DA now active in 2026, your own records must align with what exchanges report to the IRS. Discrepancies between the two will trigger IRS scrutiny. For every Bitcoin to Ethereum conversion you make, you need to document the following.

For the Bitcoin you disposed of: The exact date you originally purchased it The price you paid . including any fees The exchange or platform where you bought it Any previous transfers that might affect the cost basis

For the swap itself: The exact date and time of the conversion The fair market value of Bitcoin at the moment of the swap in US dollars The amount of Ethereum received Any fees paid on the swap The name of the exchange or protocol where the swap occurred

For the Ethereum you received: Record the cost basis as the fair market value of Bitcoin at the swap date Store this alongside your Ethereum holdings for future sale calculations

The easiest way to maintain these records is through dedicated crypto tax software. Koinly, CoinLedger, and TaxBit all connect directly to major exchanges and automatically generate the records you need. For DEX activity, Koinly’s on-chain transaction tracking is the most comprehensive option available in 2026.

- Three Legal Ways to Reduce Your Tax on Crypto Conversions

Knowing that the tax is real and unavoidable, the next logical question is how to minimize it legally. These three strategies are legitimate, widely used, and directly applicable to Bitcoin to Ethereum conversions.

Strategy 1. . Wait Past the 12-Month Mark

This is the simplest and most powerful single decision available to any crypto investor. If you are at month 10 or 11 of holding Bitcoin and you are thinking about converting, run the numbers on what waiting two more months would save you. On larger positions the difference can be tens of thousands of dollars. There is no trick involved — it simply requires patience.

Strategy 2. Offset With Losses From Other Positions

If you hold other cryptocurrencies that are currently trading below your cost basis, selling those at a loss before or in the same tax year as your Bitcoin conversion creates capital losses that offset your gain. This strategy is called tax-loss harvesting and it is particularly powerful in crypto because as of May 2026 . the wash sale rule does not apply to cryptocurrency. You can sell an altcoin at a loss, immediately buy it back, and still claim the loss against your Bitcoin gain.

If you have a $46,000 capital gain from converting Bitcoin and you harvest $18,000 in losses from underperforming altcoins in the same year, your net taxable gain drops to $27,000. On a 15 percent long-term rate that saves $2,700 in federal tax.

Strategy 3. Convert Inside a Tax-Advantaged Account

Certain self-directed IRAs allow cryptocurrency holdings. If your Bitcoin is held inside a Roth IRA, converting it to Ethereum is not a taxable event .gains inside a Roth IRA grow completely tax-free. This eliminates the capital gain calculation entirely. Setting up a crypto-capable self-directed IRA requires working with a specialized custodian and has contribution limits, but for long-term investors building significant positions it is one of the most structurally powerful options available.

- DeFi Swaps .Are They Different From Exchange Swaps?

This is a question that comes up constantly, especially among investors who use Uniswap, Curve, or other decentralized protocols rather than centralized exchanges like Coinbase or Kraken.

The short answer is no . the tax treatment is identical. The IRS taxes the economic reality of the transaction, not the platform it happens on. Swapping Bitcoin-wrapped tokens for ETH on Uniswap creates the same taxable event as swapping BTC for ETH on Coinbase.

The practical difference in 2026 is reporting. Centralized exchanges now report your transactions via Form 1099-DA. Decentralized exchanges are currently exempt from this reporting requirement following regulatory rollbacks earlier in 2026. However, the IRS still expects you to self-report every DEX swap. The absence of a 1099-DA does not mean the transaction is untaxed . it means you are personally responsible for the calculation and reporting without a safety net.

There is also a specific wrapping issue worth noting. Converting ETH to wrapped ETH (WETH) to interact with certain DeFi protocols technically creates a reporting requirement under current IRS guidance, though enforcement on this specific activity remains unclear. If you have significant WETH activity, consult a crypto-specialized CPA before filing.

- What Most People Get Wrong About This Rule

After researching this topic and speaking with investors who have received IRS notices, the same misunderstandings appear repeatedly. These are the beliefs that cost people real money.

Misunderstanding 1 “I did not make any real money because I am still in crypto”

This is the most common objection. The IRS position is that you realized a gain the moment you disposed of the Bitcoin — regardless of what you received or what happened to Ethereum afterward. If Ethereum drops 40 percent after your swap, your Bitcoin capital gain is still the same. The tax is calculated at the moment of the swap, not at the moment you eventually sell the Ethereum.

Misunderstanding 2 “Small swaps are not worth reporting”

There is no minimum threshold for crypto capital gain reporting in the US. A $200 gain on a small BTC to ETH swap is reportable. With Form 1099-DA now in effect, small swaps on centralized exchanges will appear in IRS records whether you report them or not.

Misunderstanding 3 .”I already paid fees so I should not owe tax”

Transaction fees reduce your gain. they do not eliminate the taxable event. Your fees are deducted from the proceeds or added to the cost basis, which lowers the final gain calculation. They are a benefit, not a tax exemption.

Misunderstanding 4, “Only exchanges in the US report to the IRS”

US taxpayers are required to report worldwide crypto income regardless of which country’s exchange they use. If you used a foreign exchange and believe the IRS cannot see it, that assumption carries significant legal risk. particularly as international tax information sharing agreements continue to expand.

- Frequently Asked Questions

Q: If I convert Bitcoin to a stablecoin like USDC instead of Ethereum, is that also a taxable event?

A: Yes. Converting Bitcoin to any other crypto asset .including stablecoins like USDC, USDT, or DAI .is a taxable disposal of Bitcoin at its fair market value. The fact that USDC is pegged to one dollar does not change the tax treatment of the Bitcoin you gave up.

Q: What if my Bitcoin swap resulted in a loss. do I still need to report it?

A: Yes, and you should want to. Capital losses from crypto conversions can offset capital gains from other transactions, reducing your overall tax bill. A loss from converting BTC to ETH at a bad time is still reportable on Schedule D — and it works in your favor by lowering your net taxable gain for the year.

Q: I converted Bitcoin to Ethereum two years ago and never reported it. What should I do?

A: Consult a CPA or tax professional immediately. The IRS has a three-year statute of limitations on assessment for returns filed in good faith, and six years if income was substantially underreported. Voluntary correction through an amended return is almost always preferable to waiting for the IRS to find the discrepancy, particularly now that 1099-DA reporting is active.

Q: Does the Bitcoin to Ethereum conversion affect my state taxes as well as federal?

A: Yes in most states. Most US states that have an income tax also tax capital gains at the state level, either at a flat rate or as ordinary income. California, New York, and New Jersey tax capital gains as regular income with no preferential long-term rate. If you live in a high-tax state, your effective rate on a short-term crypto conversion gain can exceed 50 percent when federal and state rates are combined.

Q: If I received the Ethereum as part of a DeFi liquidity provision rather than a direct swap, is it still taxed the same way?

A: Generally yes, though DeFi taxation has specific nuances. Providing liquidity to an AMM by depositing Bitcoin typically triggers a taxable swap event. Receiving LP tokens in return creates a new cost basis at the time of receipt. When you withdraw from the pool and receive Ethereum back, another taxable event may occur depending on the value difference. DeFi positions with significant value should always be reviewed with a crypto-specialized CPA.

Final Thoughts

Converting Bitcoin to Ethereum feels like a simple portfolio adjustment .moving from one asset to another without ever leaving the crypto ecosystem. But from the IRS perspective, the moment you gave up your Bitcoin, you triggered a taxable event that requires calculation, documentation, and reporting.

The investors who handle this correctly are not necessarily those who avoid the tax .they are the ones who plan around it. They time their swaps past the 12-month mark. They harvest losses from weaker positions to offset gains. They keep complete records throughout the year rather than scrambling at tax time.

The capital gain from a Bitcoin to Ethereum conversion is real, it is reportable, and in 2026 it is more visible to the IRS than it has ever been. Understanding exactly how it works is the first step toward managing it intelligently.

Author Note

A Note From Muhammad Qaisar, Capigain.top:

The moment that made this topic click for me personally was realizing that the IRS is not asking whether you received dollars ; it is asking whether your Bitcoin’s value went up while you held it. That shift in framing changes everything. You are not being taxed on the swap. You are being taxed on the appreciation that accumulated during your holding period. The swap simply became the moment when that gain was crystallized. Once I understood that, the entire rule made logical sense. even if it still feels counterintuitive the first time you encounter it. If you have questions about your specific situation, please speak with a qualified CPA. If you have general questions about how capital gains work across different asset types, the Contact page is always open.

Disclaimer

This article is provided for informational and educational purposes only. It does not constitute tax, legal, financial, or investment advice. Tax laws change frequently and the information presented reflects the author’s understanding of US federal tax treatment as of May 2026. Individual tax situations vary based on income, filing status, state of residence, and the specific nature of each transaction. The IRS treatment of DeFi activities and certain crypto transactions continues to evolve. Always consult a qualified and licensed tax professional or CPA before making any tax-related decision. The author and Capigain.top accept no liability for decisions made based on this content.

Muhammad Qaisar is the founder and lead researcher at Capigain.top, a financial education platform dedicated to helping everyday people understand capital gains across cryptocurrency, real estate, gold, and agricultural investments. With a passion for making complex financial topics simple and accessible, Muhammad writes in-depth, research-backed guides that help readers make smarter investment decisions. He believes that financial knowledge should be available to everyone, not just experts.

1 thought on “What Happens to Your Crypto Capital Gain When You Convert Bitcoin to Ethereum? (2026 IRS Rules)”