Gold has quietly turned ordinary people into serious wealth builders — not through luck, but through a simple strategy: buy at the right time, hold with patience, and sell with purpose. In 2025 alone, gold prices climbed over 60%, handing long-term holders one of the strongest capital gains of the decade. But here is the part most people miss — knowing how to make capital gains from gold is a skill, not a gamble.

Whether you are just starting out or you have a small amount sitting in savings wondering where to put it, this guide will walk you through exactly how buying and selling gold can build real, measurable capital gains. No complicated jargon. No confusing charts. Just clear steps, real numbers, and honest insights.

Table of Contents

- What Is a Gold Capital Gain?

- Why Gold Produces Capital Gains: The Core Logic

- 5 Main Ways to Buy Gold for Capital Gain

- Step-by-Step: How to Make Capital Gains Buying and Selling Gold

- The Holding Period — Why Timing Changes Everything

- 3 Smart Strategies That Maximize Your Gold Capital Gain

- 5 Common Mistakes That Kill Your Capital Gain

- A Real-World Example: From $5,000 to $9,400

- Frequently Asked Questions

1. What Is a Gold Capital Gain?

A capital gain is the profit you earn when you sell an asset for more than you paid for it. Gold is one of the oldest and most reliable assets for producing capital gains, and the formula is refreshingly simple:

Core FormulaCapital Gain = Selling Price − Purchase Price − Any Fees

Example: You buy 1 ounce of gold for $2,200. Three years later, you sell it for $3,800. Your capital gain is$1,600— before any applicable taxes.

Unlike rental income or business profits, a capital gain on gold is only realised the moment you actually sell. While you hold gold, its value can rise every single day — but you do not owe anything until you choose to sell. This gives investors complete control over when they take their profit.

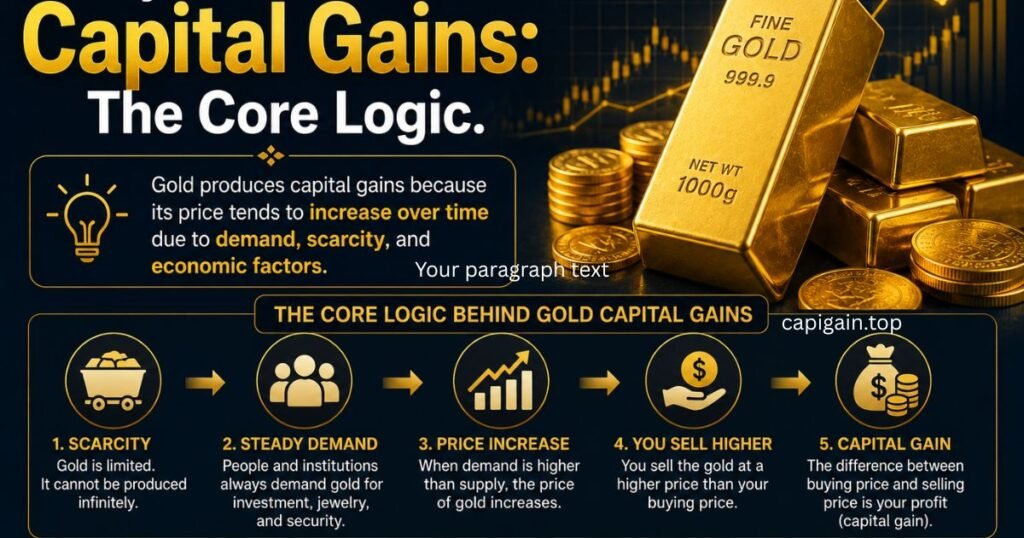

2. Why Gold Produces Capital Gains: The Core Logic

Gold does not pay dividends. It earns no interest. So why do millions of investors around the world buy it specifically to build wealth? Because gold operates on a different set of economic rules . and those rules have been consistent for over five thousand years.

Gold Rises When Currencies Weaken

Every major currency in the world can be printed in unlimited quantities by governments. Gold cannot be printed. There is a fixed amount of it in the earth. When central banks create more money . through stimulus programs, debt spending, or quantitative easing . the purchasing power of each dollar, euro, or pound falls. Gold, being scarce, rises in response. This is the single biggest driver of gold’s long-term capital gain performance.

Gold Rises During Uncertainty

Wars, pandemics, banking crises, political instability . during every major period of global uncertainty in modern history, gold prices have moved higher. Investors worldwide treat it as a financial safe harbour. The more fear in the market, the stronger the demand for gold, and the larger the potential capital gain for those who bought before the fear arrived.

Gold Demand Has Structural Support in 2026

Central banks across the world .particularly in China, India, and emerging markets ,have been buying gold at record levels to reduce their dependence on the US dollar. This structural shift in demand provides a powerful floor under gold prices and increases the long-term capital gain outlook for individual investors who position themselves early.

3. Five Main Ways to Buy Gold for Capital Gain

Not all gold investments work the same way. Each has different costs, risks, and capital gain potential. Understanding your options is the first step to making smart decisions.

| Gold Type | What You Own | Capital Gain Potential | Best For |

|---|---|---|---|

| Physical Gold Bars | Real gold you can hold | High — tracks gold price directly | Long-term holders, large amounts |

| Gold Coins | Minted gold coins (Eagles, Maple Leafs) | High + potential collector premium | Beginners, smaller budgets |

| Gold ETFs | Shares tracking gold price | Medium-High — no storage needed | Convenience seekers, frequent traders |

| Gold Mining Stocks | Shares in gold-producing companies | Very High (with more risk) | Growth-oriented, risk-tolerant investors |

| Gold Jewellery | Wearable gold items | Lower — high markups reduce net gain | Cultural buyers, long-term family wealth |

Beginner TipIf you are just starting out,government-minted gold coins(such as American Gold Eagles or Canadian Maple Leafs) offer the best balance of simplicity, liquidity, and capital gain potential. They are universally recognised, easy to buy, and straightforward to sell when your profit target is reached.

4. Step-by-Step: How to Make Capital Gains Buying and Selling Gold

Capital gains from gold do not happen by accident. They follow a clear process. Here is exactly how to approach it, from your first dollar to your first realised profit.

- Set Your Capital Gain Goal Before You Buy

Decide in advance how much profit you want to make and over what timeframe. Are you aiming for a 20% gain in two years, or a 50% gain over five years? Having a clear target stops you from making emotional decisions when prices fluctuate. Write it down. Treat it like a business decision. - Choose Your Gold Type Based on Your Budget

Under $500: Start with a fractional gold coin (1/10 oz). Between $500–$2,000: Consider a 1 oz gold coin. Over $2,000: Look at gold bars for better value per ounce, or a combination of coins and a gold ETF for flexibility. - Buy From a Reputable, Verified Dealer

Only buy from authorised mints, government-certified dealers, or reputable online platforms with strong verified reviews. Verify the gold’s purity certificate. Counterfeits do exist and buying from an unverified source eliminates your capital gain before you even start. - Record Your Purchase Details Precisely

Keep a written record of the date of purchase, price per ounce, total amount paid, and any fees. This is your cost basis — the number you will subtract from your selling price to calculate your capital gain. Without accurate records, you cannot accurately measure your profit. - Store Your Gold Securely

Physical gold must be stored safely. Options include a home safe, a bank safety deposit box, or a professional gold depository. If you are using an ETF, your gold is held digitally with no storage concern. Poor storage that leads to theft or loss permanently destroys your capital gain. - Monitor Gold Prices — But Do Not Obsess

Check gold prices weekly, not hourly. Gold is a long-term asset. Daily checking creates anxiety and often leads to panic selling at exactly the wrong moment. Set a price alert for when gold reaches your target selling price and then let time do the work. - Sell at Your Target Price, Not Your Emotion

When gold reaches your predetermined target, sell. Do not get greedy waiting for an even higher price. Lock in your capital gain. If you believe gold will continue rising, sell a portion and hold the rest — this way you secure a guaranteed profit while staying invested in future gains.

5. The Holding Period — Why Timing Changes Everything

One of the most important decisions you will make as a gold investor is not when to sell — it is how long to hold before you sell. The holding period does not just affect your tax bill. It fundamentally determines the size of your capital gain.

Short-Term Holding (Under 12 Months)

Buying and selling gold within a year is possible, but it is the riskiest approach for capital gain. Gold prices in the short term can move sideways or even dip temporarily, meaning you could sell at a loss. Additionally, in the United States, profits from assets held under one year are taxed at ordinary income rates — which can reach as high as 37% — significantly reducing your net gain.

Long-Term Holding (Over 12 Months)

Holding gold for more than one year triggers long-term capital gain treatment in most jurisdictions. For physical gold in the US, this means a maximum tax rate of 28% — often lower than the short-term rate. More importantly, historical data consistently shows that gold held for three to five years produces far greater average gains than gold held for months.

| Holding Period | Average Historical Gain* | Tax Treatment (US) | Risk Level |

|---|---|---|---|

| Under 6 months | Unpredictable (could be negative) | Ordinary income rate (up to 37%) | High |

| 6–12 months | 3% to 12% average | Ordinary income rate (up to 37%) | Medium-High |

| 1–3 years | 10% to 35% average | Long-term collectibles rate (max 28%) | Medium |

| 3–5 years | 25% to 80% average | Long-term collectibles rate (max 28%) | Low-Medium |

| 5+ years | 50% to 200%+ in bull cycles | Long-term collectibles rate (max 28%) | Low |

*Historical averages based on gold price data. Past performance does not guarantee future results.

6. Three Smart Strategies That Maximise Your Gold Capital Gain

Strategy 1: Dollar-Cost Averaging (DCA)

Instead of trying to time the perfect moment to buy gold, invest a fixed amount at regular intervals — say, $200 every month. Some months you buy when prices are high. Other months you buy when prices are low. Over time, your average purchase price smooths out, and your overall capital gain position tends to be stronger than someone who tried to “time the market” and guessed wrong.

This strategy is particularly powerful for beginners because it removes the paralysis of trying to predict gold prices. You simply invest consistently and let compounding time do the work.

Strategy 2: Buy the Dip, Sell the Peak

Gold regularly experiences temporary price corrections of 5% to 15%, even during long-term bull markets. These dips are not danger signals — they are buying opportunities. Experienced gold investors keep a portion of their capital reserved specifically to add to their gold holdings during these corrections, dramatically improving their average entry price and magnifying their eventual capital gain when prices recover and move higher.

Strategy 3: Layer Your Gold Types

Sophisticated investors do not hold only one type of gold. They layer their investments: physical coins or bars for long-term wealth preservation, a gold ETF for liquidity and easy trading, and occasionally gold mining stocks for amplified upside when gold is in a strong bull market. This layering approach lets you take partial capital gains from the more liquid parts of your portfolio while maintaining your core long-term gold position.

7. Five Common Mistakes That Kill Your Capital Gain

Many beginners make the same avoidable errors. Understanding these mistakes before you invest is worth more than any gold price prediction.

- Panic selling during temporary dips. Gold regularly drops 5–10% before resuming its upward trend. Selling during these dips locks in a loss. The investors who build the largest capital gains are those who hold through short-term volatility.

- Buying gold jewellery expecting high capital gains. Jewellery carries a significant markup from the jeweller — sometimes 50% to 200% over the actual gold value. When you sell, you receive only the melt value of the gold. The jeweller’s markup is a cost, not a capital gain.

- Not keeping purchase records. Without precise records of what you paid, when, and what fees were involved, you cannot accurately calculate your capital gain. You may also overpay on taxes by understating your cost basis.

- Buying from unverified sellers. Counterfeit gold exists, particularly in the form of gold-plated bars and coins. Always buy from authorised, certified dealers. Buying counterfeit gold produces zero capital gain — it produces a total loss.

- Putting all savings into gold. Gold is a capital gain tool, not a complete financial plan. Most financial experts suggest keeping gold as 5–15% of an overall investment portfolio. Over-concentration in any single asset increases risk without proportionally increasing expected returns.

8. A Real-World Example: From $5,000 to $9,400

Let us put all of this into a concrete, realistic scenario to show exactly how gold capital gains work in practice.

Real Scenario WalkthroughJanuary 2022:An investor named Marcus decides to invest $5,000 in gold. He uses the dollar-cost averaging strategy, splitting his purchase across three months. His average purchase price works out to approximately $1,850 per ounce. He buys 2.7 ounces of physical gold coins from a certified dealer and stores them in a home safe.

His records show:2.7 oz × $1,850 = $4,995 total cost (plus $80 in dealer fees = $5,075 total cost basis)

February 2025:Gold reaches $2,900 per ounce. Marcus sells his 2.7 ounces.

Selling proceeds:2.7 oz × $2,900 = $7,830

Capital Gain:$7,830 − $5,075 =$2,755 profit (54.3% gain over 3 years)

Because Marcus held his gold for over one year, his gain qualifies for long-term capital gain treatment. Depending on his income bracket, his tax rate is significantly lower than it would have been for a short-term gain.

This is not a speculative scenario. Gold rose from approximately $1,800 in early 2022 to above $2,900 in early 2025. Investors who followed a simple buy-and-hold strategy during this period achieved exactly this kind of capital gain — without any trading expertise, market timing, or complicated financial instruments.

Important Disclaimer:

This article is for informational and educational purposes only. It does not constitute financial, investment, or tax advice. Gold prices fluctuate and past performance does not guarantee future results. Capital gain tax rules vary by country and individual circumstances. Always consult a qualified financial advisor and tax professional before making investment decisions.

Frequently Asked Questions

How do you make a capital gain from gold?

You make a capital gain from gold when you sell it for more than you paid for it. If you buy gold at $2,000 per ounce and later sell it at $2,800, your capital gain is $800 per ounce. The key is purchasing at a lower price point and selling after the market has moved higher. The longer you hold, the more consistently gold produces meaningful gains based on historical data.

How long should I hold gold to get the best capital gain?

Most financial experts recommend holding gold for at least one full year to qualify for more favourable long-term capital gain tax treatment. However, for the strongest average returns, gold held for three to five years has historically produced the most reliable capital gains. The longer the hold, the more time gold has to move through a full price cycle and reach significantly higher levels.

Is physical gold or a gold ETF better for capital gains?

Both physical gold and gold ETFs closely track the gold price, so their capital gain potential is similar. Physical gold gives you direct, tangible ownership with no counterparty risk, but it requires secure storage. Gold ETFs are simpler to buy and sell through a brokerage account. For beginners who want ease of access, a gold ETF is often more practical. For those who want true ownership, physical gold coins or bars are the preferred option.

What is the best time to buy gold for capital gain?

There is no single “perfect” time to buy gold, which is why dollar-cost averaging — buying small amounts at regular intervals — is the recommended approach for most people. However, gold historically offers strong entry points during periods of relative market calm before uncertainty rises, when interest rates are declining, and when gold prices are pulling back temporarily from recent highs. Buying during a 5–10% correction in an otherwise upward trend has historically produced excellent capital gains.

Can I lose money buying and selling gold?

Yes. If you sell gold for less than you paid, you have a capital loss rather than a capital gain. Gold prices do fluctuate, and short-term trading carries significant risk of loss. The most common cause of loss for gold investors is panic-selling during temporary price dips. A patient, long-term approach with a clear target selling price significantly reduces the probability of experiencing a loss.

Do I have to pay tax on gold capital gains?

In the United States, the IRS classifies physical gold as a collectible, and long-term capital gains on collectibles are taxed at a maximum rate of 28%. Short-term gains (assets held under one year) are taxed at ordinary income rates, which can reach 37%. Tax treatment varies significantly by country, so it is strongly advisable to consult a qualified tax professional in your region to understand your specific obligations before buying or selling gold.

How much gold should a beginner buy to start earning capital gains?

There is no required minimum. Many investors begin with a single fractional gold coin (1/10 oz) for under $500. What matters more than the starting amount is consistency — buying regularly, keeping records, and holding with patience. Starting small, learning the process, and gradually increasing your position as you gain confidence is a far smarter approach than waiting until you can make a large lump-sum investment.

Final Thoughts: Gold Capital Gains Are Built, Not Found

Making capital gains from buying and selling gold is not complicated — but it does require clarity, patience, and a plan. The investors who consistently build wealth through gold are not the ones chasing daily price movements. They are the ones who buy with a clear purpose, hold through the inevitable short-term noise, and sell when their target is reached.

Gold has been a reliable store of value and a wealth-building tool for thousands of years. In 2026, with central banks buying at record levels, inflation concerns persisting, and global uncertainty remaining elevated, the fundamental conditions that drive gold capital gains remain firmly in place.

Start with what you have. Choose a reputable dealer. Keep your records. Stay with us for capigain tips.

Muhammad Qaisar is the founder and lead researcher at Capigain.top, a financial education platform dedicated to helping everyday people understand capital gains across cryptocurrency, real estate, gold, and agricultural investments. With a passion for making complex financial topics simple and accessible, Muhammad writes in-depth, research-backed guides that help readers make smarter investment decisions. He believes that financial knowledge should be available to everyone, not just experts.