Gold had one of its most dramatic years on record in early 2026.how much gold should a beginner buy The price of gold hit an all-time high of $5,608 per ounce in January 2026, before pulling back. Gold is trading near $4,800 per ounce as of April 2026, roughly 14% below its all time high of $5,589.38 set on January 28, 2026. For small investors watching those numbers, the question of how much to buy .and whether now is even the right time feels more urgent than ever.

This guide answers that question practically, with real dollar examples across four different budget levels, a breakdown of how capital gain actually works in gold, and the specific mistakes that cause most beginners to lose money before they ever make it.

What This Guide Covers

- What Is Capital Gain From Gold . Simply Explained

- How Much Gold Should a Beginner Actually Buy in 2026?

- Four Budget Scenarios With Real Numbers

- The Dollar-Cost Averaging Strategy — Why It Beats Lump-Sum for Beginners

- Does Buying More Gold Always Mean More Capital Gain?

- Five Mistakes That Destroy a Beginner’s Capital Gain

- The Best Way to Start With a Small Budget in 2026

- Frequently Asked Questions

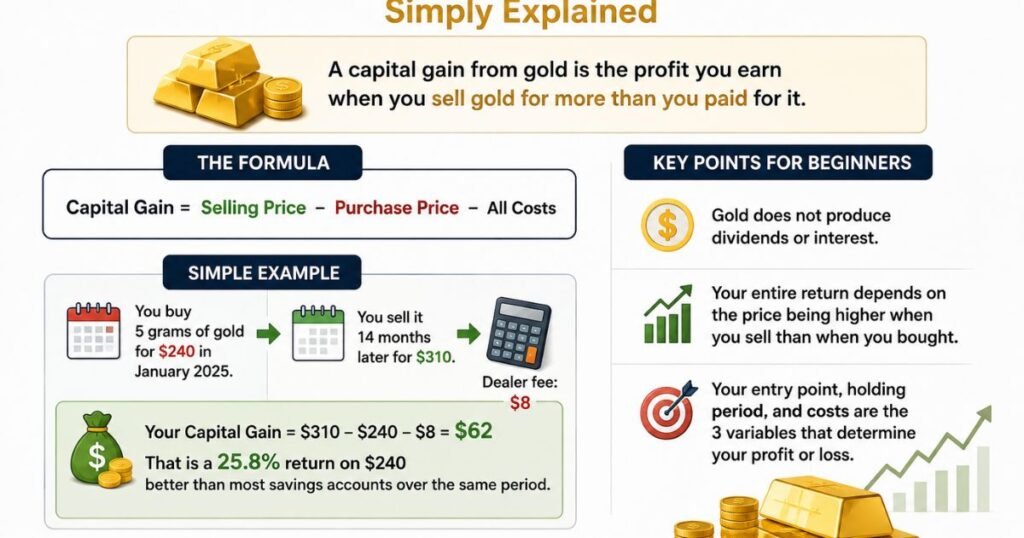

1. What Is Capital Gain From Gold . Simply Explained

Before deciding how much gold to buy, it is worth being clear on exactly what you are trying to achieve. A capital gain from gold is straightforward: it is the profit you earn when you sell gold for more than you paid for it.

The Formula:

Capital Gain = Selling Price . Purchase Price, All Costs

Simple Example:

You buy 5 grams of gold for $240 in January 2025.

You sell it 14 months later for $310.

Dealer fee: $8

Your Capital Gain = $310 − $240 − $8 = $62

That is a 25.8% return on $240 . better than most savings accounts over the same period.

The key nuance for beginners is that gold does not produce dividends or interest. Your entire return depends on the price being higher when you sell than when you bought. This makes your entry point, your holding period, and your costs the three variables that determine whether you earn a capital gain or absorb a loss.

2. How Much Gold Should a Beginner Actually Buy in 2026?

The professional consensus on this question is remarkably consistent. A common approach experts recommend is allocating just 5–10% of your portfolio to gold. This gives you upside and inflation hedging while allowing you to spread your capital across other investments.

The recommendation to hold 5% to 15% in gold is not arbitrary. It comes from decades of portfolio research showing that a modest gold allocation improves risk-adjusted returns over time without dragging down overall performance during strong equity markets.

In practice, that translates to something very specific for most beginners:

| Total Savings Available | Suggested Gold Allocation (5–10%) | What That Buys (at $4,800/oz) |

|---|---|---|

| $500 | $25 – $50 | Fractional gold ETF shares |

| $2,000 | $100 – $200 | 1–2g physical coin or ETF shares |

| $5,000 | $250 – $500 | 2–5g coin, or ETF position |

| $10,000 | $500 – $1,000 | 1/10 oz coin + ETF allocation |

| $20,000 | $1,000 – $2,000 | Multiple fractional coins or bars |

The reason this range matters more than a fixed number is simple: a beginner who puts 40% of their savings into gold has very little financial flexibility when life presents unexpected expenses. Selling gold under pressure. at an inconvenient time, before the price has recovered ,is one of the most reliable ways to turn a paper gain into a real loss.

The Rule That Changes How You Think About This:

Only invest in gold the money you genuinely do not need for at least 12 to 24 months. Gold is not a liquid emergency fund. If you may need the money for rent, medical bills, or a planned purchase within a year, that money should stay in cash, not gold. The capital gain from gold rewards patience, not urgency.

3. Four Budget Scenarios. Real Numbers for Real Beginners

Abstract percentages are helpful for framing, but most people need to see actual scenarios to make a real decision. Here are four realistic examples across different budget levels, using current 2026 conditions.

Scenario 1: The $300 Starter (Very Small Budget)

- Investment: $300 in a Gold ETF (e.g., IAUM at 0.09% annual fee)

- Gold price at purchase (Jan 2025): ~$2,650/oz

- Gold price at sale (Jan 2026): ~$2,750/oz (+3.8%)

- Annual ETF fee: ~$0.27

- Gross gain: $11.40

- Net capital gain after fee: ~$11.13

A small return in dollar terms, but the habit of regular investing formed here is worth far more than $11. This scenario is about building discipline, not wealth.

2. Scenario.

The $1,000 First Purchase

- Investment: $1,000 in a 1/5 oz American Gold Eagle coin

- Purchased: January 2023 at ~$1,920/oz spot (+6% premium = $2,035 paid)

- Sold: May 2026 at ~$4,800/oz spot (dealer offers 95% of spot = $4,560)

- Gold weight held: 1/5 oz = $912 worth in 2023 at spot

- Value at sale: 1/5 oz × $4,800 × 0.95 = $912 → $912 × (4800/1920) × 0.95 ≈ $2,280

- Net capital gain: $2,280 − $1,000 = ~$1,280 gain on $1,000 invested (+128%)

This scenario reflects the actual 2023–2026 gold rally. Investors who bought in 2023 and held through 2026 earned exceptional returns , but required patience through a volatile middle period in 2024.

3 Scenario .

Monthly $100 Investment (Dollar-Cost Averaging)

- Strategy: $100/month into a Gold ETF 12 months

- Total invested: $1,200

- Average entry price (smoothed across 12 months): Varied .avoids single bad entry

- Assumed 15% gain over the 12-month period (conservative):

- Portfolio value after 12 months: ~$1,380

- Net capital gain: ~$180 on $1,200 invested

This is the approach most financial advisors recommend for beginners. It removes the pressure of trying to time the market and produces consistent, predictable exposure to gold price movements over time.

4. Scenario.

The Concentrated Bet (What to Avoid)

- Investment: $5,000 all-in at $5,589/oz (January 2026 peak)

- Gold price 4 months later (May 2026): ~$4,800/oz (−14%)

- Current portfolio value: ~$4,300

- Unrealized loss: −$700 (−14%)

This investor is not permanently damaged. Gold may recover and surpass $5,589 again. But if they need that money now or panic-sell, the loss becomes permanent. Concentrating a large sum at a single price point is the most common and costly beginner mistake in gold investing.

4. The Dollar Cost Averaging Strategy. Why It Beats Lump Sum for Beginners

Dollar-cost averaging removes the emotional decision entirely. You buy a fixed dollar amount at regular intervals. Some months you buy high, some low. Over time, your average entry reflects the genuine trend. not the anxiety of a single moment.

For a beginner trying to earn capital gain from gold, this matters for three specific reasons:

- It eliminates the impossible task of timing the market. Even professional gold traders cannot reliably predict the best entry point. Regular monthly purchases remove this pressure entirely.

- It builds a position gradually without large capital commitment. Starting with $50–$100 per month is a legitimate, professional-grade strategy. not a compromise you make because you cannot afford more.

- It protects you from the worst entry points. An investor who bought $200 per month from January through December 2025 would have a blended entry price that reflects the full range of that year. not just the expensive months.

✅ DCA Starter Plan. For Any Budget:

| Monthly Budget | Best Vehicle | Year 1 Total | At 15% Annual Gain |

|---|---|---|---|

| $50 / month | Gold ETF (GLDM/IAUM) | $600 | ~$690 |

| $100 / month | Gold ETF (GLDM/IAUM) | $1,200 | ~$1,380 |

| $200 / month | ETF + occasional coin | $2,400 | ~$2,760 |

| $500 / month | ETF + fractional coins | $6,000 | ~$6,900 |

15% annual gain used for illustration only. Past performance does not guarantee future results. See disclaimer below.

5. Does Buying More Gold Always Mean More Capital Gain?

The instinct that “more gold = more profit” is logical on the surface but breaks down in practice for one important reason: the percentage return is identical regardless of position size. What changes is the scale of both your gain and your potential loss.

| Investment Amount | Gold Gains 20% | Gold Falls 15% |

|---|---|---|

| $500 | +$100 | −$75 |

| $2,000 | +$400 | −$300 |

| $5,000 | +$1,000 | −$750 |

| $10,000 | +$2,000 | −$1,500 |

The percentage return is the same in every row. What scales with the investment size is the impact on your overall financial life when the market moves against you. A $75 loss on a $500 investment is an inconvenience. A $1,500 loss on a $10,000 investment . representing a large portion of someone’s savings . can trigger a panic sell at exactly the wrong moment, turning a temporary price dip into a permanent realized loss.

This is why the right amount of gold for a beginner is not the maximum amount you could technically afford. It is the amount you could watch drop 15% in value and still leave untouched, knowing the long-term trend supports recovery.

6. Five Mistakes That Destroy a Beginner’s Capital Gain in Gold

These are the patterns that consistently separate investors who earn capital gain from those who do not . not because of luck, but because of avoidable structural errors.

#1 Mistake: Investing All Available Capital at Once

Putting your full savings into gold at a single entry point eliminates the protection that dollar-cost averaging provides. Gold hit $5,589 in January 2026 and has since corrected roughly 14%. Anyone who invested everything at that peak is now sitting on a 14% unrealized loss not because they chose the wrong asset, but because they chose the wrong entry strategy.

#2 Mistake: Buying When Prices Are Already Making Headlines

The moment gold is trending on financial news, retail investors rush in near the peak. This is precisely backwards from how capital gain is earned. The better approach is to build a position steadily. including during quiet periods when gold is not making headlines . rather than reacting to price spikes.

#3 Mistake: Expecting Short-Term Returns From a Long-Term Asset

Gold is not a stock that can double in six months based on earnings news. Its capital gain comes from macroeconomic shifts. inflation cycles, currency debasement, and geopolitical stress. that unfold over years, not quarters. Investors who enter expecting to sell for a profit in three months are almost always disappointed, and many sell at a loss simply because they set the wrong time horizon.

#4 Mistake: Ignoring the Full Cost Stack

Physical gold comes with costs that are rarely advertised prominently: dealer premiums of 5%–8% at purchase, a spread of 3%–5% below spot when selling, storage and insurance if you hold significant amounts, and the opportunity cost of capital that earns no income while held in gold. None of these appear in the gold price chart. But all of them affect your real capital gain.

#5 Mistake : Not Setting a Sell Target Before You Buy

Most beginners buy gold with a vague intention to “sell when it goes up.” Without a specific target. For example, “I will sell when I have a 30% capital gain, or after 3 years, whichever comes first” decisions become emotional. You hold on to gains hoping for more, or panic-sell through a temporary dip. Setting the exit criteria before you enter is one of the most underrated disciplines in gold investing.

7. The Best Way to Start Investing in Gold With a Small Budget in 2026

Beginners have five primary options: physical gold (coins and bars), gold ETFs, mining stocks, futures contracts, and Gold IRAs. Most financial experts recommend allocations between 5 and 10% for general portfolios, with adjustments based on risk tolerance.

For a genuine beginner focused on earning capital gain with minimal complexity, the practical starting path in 2026 looks like this:

1. A Practical First 12 Months in Gold Investing

2. Month 1: Open a brokerage account and buy your first Gold ETF shares

Fidelity, Schwab, or any major broker. Start with GLDM or IAUM for the lowest fees. Buy whatever you can afford even $50 is a legitimate start. The goal of Month 1 is to hold a real position and watch how it moves.

Months 2–6: Add a fixed amount every month. do not change it

Set up an automatic monthly purchase if your broker allows it. Consistency matters more than amount here. $75/month invested for 6 months is $450 of gold exposure built without timing stress.

3. Month 6: Consider adding one physical gold coin to your position

Once you have ETF experience and understand how the price moves, a 1/10 oz American Gold Eagle or similar coin adds tangible ownership to your portfolio. Do not skip the ETF phase .it teaches you to hold through volatility without the complexity of physical storage.

Month 12: Review your position . not to panic-sell, but to assess

Has your allocation grown beyond 10% of your portfolio? Rebalance. Are you at your capital gain target? Consider a partial sell. Have circumstances changed? Adjust the monthly amount. Do not review monthly. it encourages emotional decisions. Annual is enough.

8. Frequently Asked Questions

What is the minimum amount of gold a beginner can buy in 2026?

Through a Gold ETF using fractional shares, you can start with as little as $1 through brokers like Fidelity or Robinhood. For physical gold, the practical minimum is a 1-gram gold coin or bar, which currently costs approximately $180–$220 depending on the dealer and premium. Most financial advisors suggest starting with whatever amount you can commit to buying consistently every month. even if it is small.

Is it too late to buy gold in 2026 after prices peaked at $5,589?

Investors who bought at “high” prices in 2023 are still significantly ahead. The lesson is not that every entry is equal. It is that in a bull market, the cost of waiting usually exceeds the cost of imperfect timing. The current pullback to around $4,800 represents a 14% correction from the peak. which historically has been a reasonable entry zone during gold bull markets, not a signal to avoid the asset.

Should a beginner buy physical gold or a gold ETF first?

For most beginners, a Gold ETF is the better starting point. It requires no storage, no insurance, no premium at purchase, and can be bought with any dollar amount. Starting with ETF shares teaches you how gold behaves without the logistical complexity of physical ownership. Once you understand how you respond to price movements,whether you hold calmly or feel pressure to sell ,you are better equipped to decide whether physical gold suits your temperament and goals.

How long should a beginner hold gold before expecting a capital gain?

The minimum holding period worth targeting is 12 months .both because gold’s capital gain tends to emerge over medium-to-long time horizons and because in the US, holding for more than one year qualifies your gain for long-term capital gain treatment rather than the higher short-term rate. Most financial advisors suggest thinking of gold as a 3–7-year position for meaningful capital gain potential, with the expectation that prices will be volatile in the short term.

Can someone with a very small budget actually earn meaningful capital gain from gold?

Yes, but the definition of “meaningful” needs to be calibrated to the investment size. On a $500 gold position, a 20% gain produces $100. That is not life-changing. But the habit, the knowledge, and the investment infrastructure you build while earning it are genuinely valuable. Many experienced gold investors started with a single fractional coin or a small ETF position and scaled steadily as their income and confidence grew. The compounding of both returns and discipline over 5–10 years is where real capital gain from gold tends to accumulate.

The Bottom Line: How Much Gold Should a Beginner Buy?

Start with 5–10% of your investable savings .

not your total wealth, just the portion you can genuinely leave untouched for at least 12 months. For most beginners, that translates to somewhere between $100 and $1,000 for a first position. The specific number matters far less than these three things: starting, staying consistent with monthly additions, and not selling the first time the price drops.

The single best structural decision a beginner can make

is to begin with a low-cost Gold ETF inside a Roth IRA, adding a fixed monthly amount. The Roth IRA shelters your capital gain from the 28% collectibles tax. The monthly contribution plan removes timing pressure entirely. And the ETF requires no storage or physical handling until you are ready to graduate to coins or bars.

Gold’s capital gain is not earned through clever timing or large initial purchases. It is earned through patience, consistent position-building, and the discipline to hold through the inevitable periods of volatility that separate beginner investors from those who actually collect meaningful returns.

Want to go deeper on building a gold capital gain strategy? These guides are your next step:

- Gold ETF vs. Physical Gold: Which Gives Better Capital Gain for Small Investors in 2026?

- How to Sell Gold Jewelry for Maximum Capital Gain — Step-by-Step Guide

A Note From Muhammad Qaisar, Capigain.top

The question that sparked this article came from a reader who wrote to ask whether $200 was “too little to bother with” when it came to gold investing. My answer then and now is that $200 is a perfectly legitimate first position,but more importantly, the person who builds a $200 habit into a $500 habit into a $1,000 habit over three years has constructed something far more valuable than the dollar amount suggests. That is the trajectory I wanted this guide to make visible. If you are at the beginning of that journey and have questions I have not answered here, the contact page is always open.

Important Disclaimer

This article is provided for informational and educational purposes only. It does not constitute financial, investment, legal, or tax advice. All examples, scenarios, and figures used in this guide are illustrative estimates intended to demonstrate concepts and should not be relied upon as predictions of future performance. Gold prices are volatile and can decline as well as rise. Past performance does not guarantee future results. The information in this article reflects general market conditions as understood in May 2026 and is subject to change. Tax treatment varies by country, individual circumstance, and applicable law. Always consult a qualified financial advisor and licensed tax professional before making any investment or financial decision. The author and Capigain.top are not licensed financial advisors and accept no liability for investment decisions made based on this content.

thanks for visiting capigain.top

Muhammad Qaisar is the founder and lead researcher at Capigain.top, a financial education platform dedicated to helping everyday people understand capital gains across cryptocurrency, real estate, gold, and agricultural investments. With a passion for making complex financial topics simple and accessible, Muhammad writes in-depth, research-backed guides that help readers make smarter investment decisions. He believes that financial knowledge should be available to everyone, not just experts.